Intro: Welcome to the Financial Thunderdome

So you’ve got a “million dollar idea.” Cute. You’ve already told your friends it’s the next Uber, but for dogs. Or maybe an app that texts your mom back for you (spoiler: VCs would 100% actually fund that one). The only Business problem? Your bank account looks like a war crime, your credit score makes landlords cry and you’ve already Venmo requested all your friends for that $7.50 they “forgot” about.

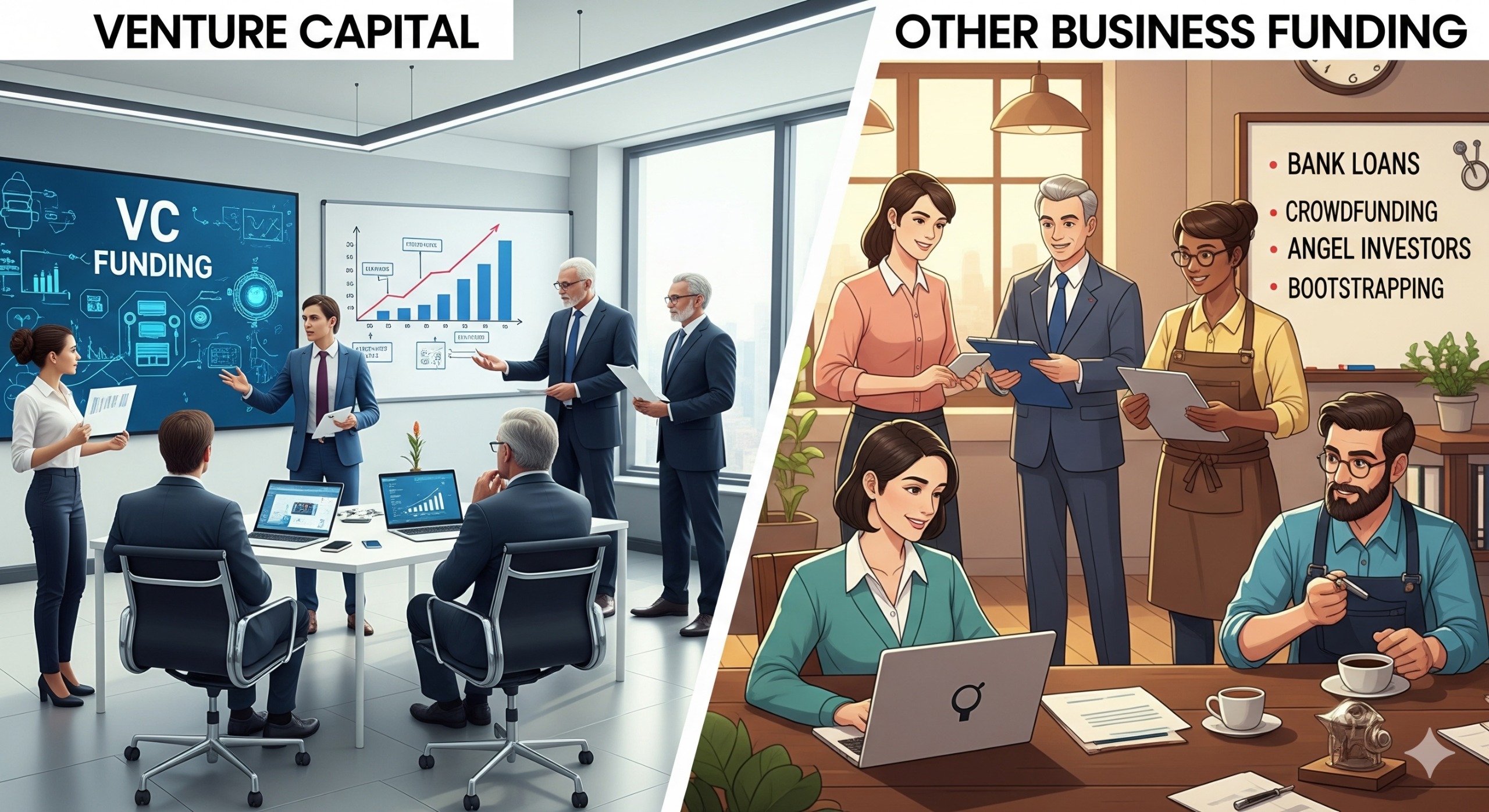

Enter the two grudging parents of capitalism: Venture Capital and Business Funding Options. One gives you money while stealing your control faster than your roommate steals cold brew; the other lets you keep your freedom while putting you on the loan payment treadmill of despair until 2064.

This blog is not here to glorify either, because newsflash: both are financial nightmares. This is your brutally relatable, sarcastic guide to the world of raising money in the U.S. Brace yourself it’s about to feel like a cross between Shark Tank and the DMV.

VCs: Glamorous Sharks or Investor Vampires?

Let’s cut the fluffy startup mic-drop speeches: venture capitalists are rich sharks with Patagonia vests and hyperinflated egos. They’ll tweet that they “support innovation,” when really they just want to double their cash flow and get bragging rights about “spotting the next unicorn.”

The VC Experience in 5 Easy Steps

- Pitch Time! You get to stand in a borrowed blazer, mumbling buzzwords like “scalable” and “disruption” while praying your slideshow loads.

- Judgement Day: They’ll ask, “What’s your five year plan?” even though you can’t plan 5 hours ahead because your Wi Fi router keeps lagging.

- Checks Fly In: If they actually like you, congrats! Enjoy their money but also kiss goodbye to absolute control of your Business.

- Creative Death: From now on, every little decision yes, even your choice of office snacks becomes something a VC “weighs in on.” Independent? Never heard of her.

- Exit, Baby:The dream is they ride your Business to IPO glory. The nightmare? They dump you like last season’s failed TikToker when you don’t “scale fast enough.”

Harsh truth: Venture capitalists aren’t angels. They’re Vegas gamblers trading chips for your blood, sweat and tears.

The Dark Romance With VCs

Here’s the trap: VCs make you feel seen. Someone with millions in the bank says “I believe in your dream.” That emotional hit? Better than your therapist telling you you’ve made “progress.” But oh baby, you pay for that validation.

- You give up equity (ownership). Translation: you’re now the co pilot on a plane you built.

- They expect insane growth like, grow 10x in 3 days or else.

- They say “we’re partners,” but really it’s “we own you until we cash out.”

Traditional Business Funding: Boring, Predictable, Soul Crushing Debt

Now let’s saunter into the dusty old world of Business Funding Options. Yup, banks, government loans, grants and the occasional sketchy uncle with “extra cash” he made flipping NFTs. Unlike VCs, they don’t want ownership but trust me, they’ll get their cut another way.

Why Banks Are the Human Version of Dial Up Internet

- The paperwork is colossal. You’ll answer more questions than in an FBI interrogation.

- They “evaluate risk.” Which really means they’re side eyeing you like a Tinder date who spotted three red flags before dessert.

- Your credit score isn’t just a number it’s literal financial Tinder swipe logic. If it sucks, you’re out.

The Misery of Repayments

Let’s be honest: banks and loan officers don’t care if your Business saves dolphins or cures hangovers. They just want guaranteed repayment. Miss a payment? Say hello to interest rates so high they could moonwalk next to Elon Musk’s rockets.

- Predictable? Yes.

- Soul numbing? Absolutely.

- Creative freedom left? Kind of, but you’ll be too poor to care.

At least banks aren’t living rent free in your Slack channel trying to micromanage logo designs. But, plot twist: you may still end up googling “how to live in a Honda Civic” when you can’t keep up with repayments.

The Epic Cage Match: VCs vs. Banks

Since America loves drama, let’s make this a UFC fight featuring your financial anguish.

Round 1: Ownership

- VCs: Hand over your equity, kid. They take a slice and “slice” might mean half.

- Banks: Keep your soul; we just want your money. Forever.

Winner: Neither. It’s like choosing between an overbearing stepdad and a nagging subscription service.

Round 2: Flexibility

- VCs: Constantly meddling in your daily life. They’re basically your new toxic boss.

- Banks: Don’t care what you do just cough up the repayments.

Winner: Banks. At least you can cry in peace without a VC asking if your tears are “scalable.”

Round 3: Long Term Pain

- VCs: Lose control of your [Business] forever. Even if you hustled yourself into burnout, it’s their win not yours.

- Banks: Chained by debt. You’ll probably have grandkids before you’re free.

Winner: Tie. Two different flavors of misery.

Millennials, Gen Z and the Myth of Financial Freedom

This is the part where all those TikTok hustle gurus scream at you to “stop being lazy and just RAISE CAPITAL.” Sure dude. Easy. Let me just manifest three extra zeroes in my PayPal account.

Reality check? Whether you go VC or bank, you’re still in capitalist jail. Don’t romanticize it. People bragging about their “Series A funding” are still secretly crying in the shower. People bragging about “low interest loans” are basically hostages of Wells Fargo.

For millennials and Gen Z, both routes are just new ways to stay broke but look glamorous doing it:

- You flex about raising $5M but live on Uber Eats coupons.

- You flex about getting a “great loan deal” but can’t sleep because of debt anxiety.

- You call yourself a “founder” but your body screams, “please go outside.”

Let’s Be Extra Sarcastic: Realistic Scenarios

Imagine you’re starting a rug cleaning company called DustBusters, LLC.

- VC Route: You pitch it as “the Uber of carpets.” Some guy in a Tesla throws $2M at you. Now he owns 40% of your company and sends you late night Slack messages about “growth hacks.”

- Bank Loan Route: You go to a bank. They look at your rug company and go “Cute, here’s $200K, but sign here promising to sell your kidneys if you miss repayments.”

Either way, you the genius founder are broke and anxiety ridden but boy, your LinkedIn? Fire.

The Stark Reality: Neither Is Your Savior

Let’s kill the dream once and for all: Venture Capital vs. Business Funding isn’t good vs. bad. It’s bad vs. differently bad. The only time either makes sense is if you’re ready to sacrifice sleep, health and possibly your entire self identity for money.

Here’s your honest cheat sheet:

- VCs are a good fit if: you want to go big and fast and don’t care if your Business doesn’t even feel like yours anymore. It’s all about fireworks and exits, baby.

- Banks are good if: you’d rather stay small to medium and can handle watching money disappear monthly for years without slamming your head against a wall.

The Pretend Inspiring Conclusion

Congrats, brave reader you actually made it this far without rage closing the tab. You now know the glamorous choice between VC overlords and bank induced debt spirals. Both have shiny marketing; both are traps.

So go forth. Pick your poison: do you want to sell off your Business piece by piece or carry it whole but with the crushing weight of debt that’ll follow you into your next reincarnation?

Either way, you’re still broke, still tired and still Googling “how to write an investor pitch deck in Canva.” But hey at least now you can rant about it at brunch.